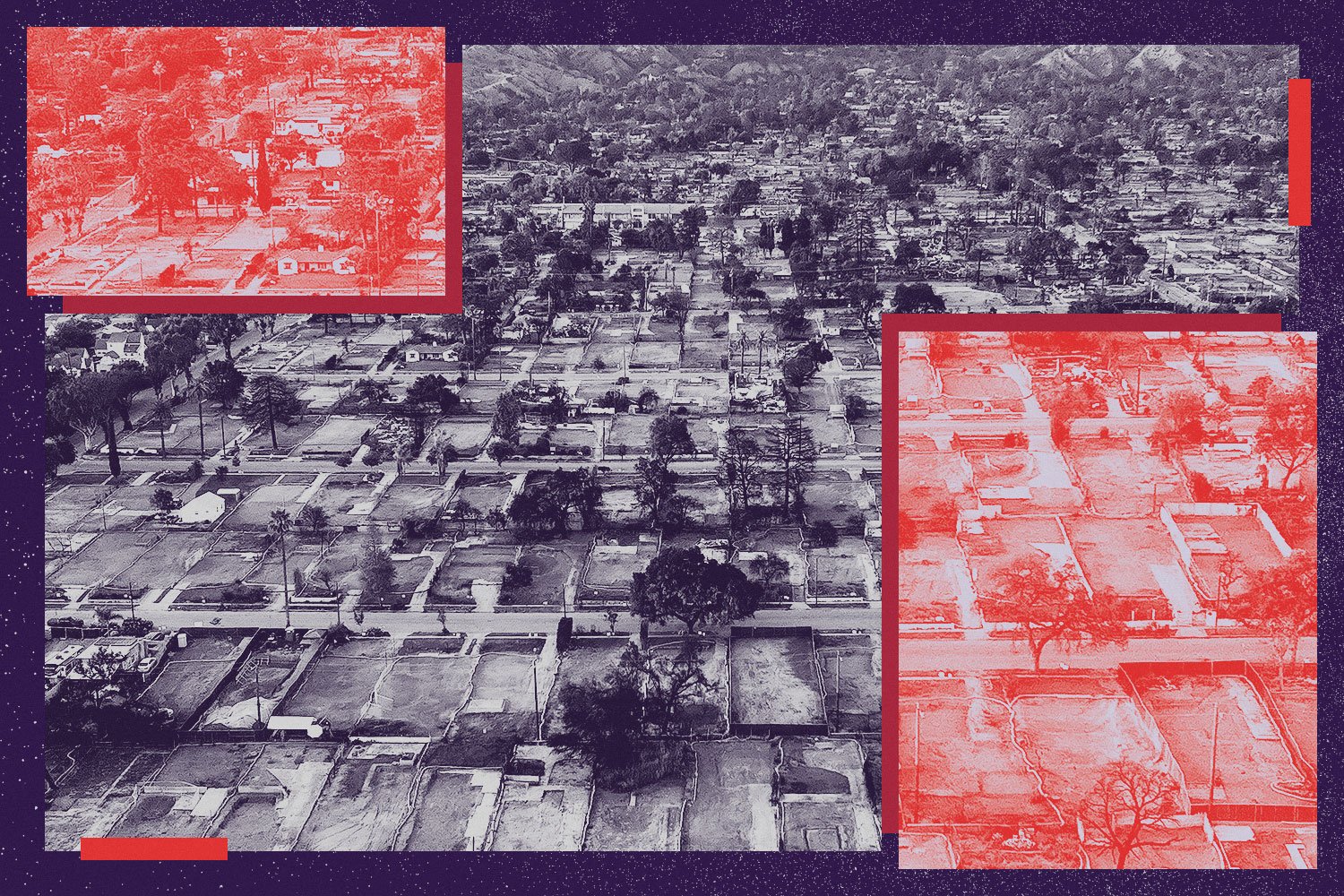

Redfin's July 2025 analysis, reported by The Real Deal, puts residential damage from the January 2025 Los Angeles wildfires at nearly $52 billion — a figure that exceeds the GDP of several U.S. states and reframes what "prime location" means in the country's most-watched luxury market. The Palisades and Eaton fires together destroyed more than 16,000 structures, and the bulk of the dollar damage concentrated in some of LA's most expensive ZIP codes: Pacific Palisades, Malibu, Altadena. The number is no longer just a disaster statistic. It has become an input into how lenders, insurers, appraisers and ultra-high-net-worth buyers price a coastal or hillside parcel.

A damage figure that redraws the map

According to Redfin's underlying analysis, the $51.7 billion residential damage estimate makes the January 2025 LA fires one of the most financially destructive wildfire events in U.S. history. Pacific Palisades alone accounted for more than half of the dollar value destroyed — a function of both the number of homes lost and the median value of those homes, many of which traded in the $4M–$20M range before the fire.

The Real Deal's coverage emphasizes that the damage is not evenly distributed across LA's luxury geography. It clusters in two specific topographies: coastal Westside (Palisades, parts of Malibu) and dry foothill (Altadena, Eaton Canyon). Both share the wildland-urban interface profile that the 2026 California WUI Code, effective January 1, now treats as the default building condition for new construction in Fire Hazard Severity Zones.

$51.7B — residential damage estimate, January 2025 LA wildfires (Redfin)

16,000+ — structures destroyed across Palisades and Eaton fires

Up to 50% — wildfire premium discount available to IBHS-certified homes through participating carriers

From "safe address" to "insurable address"

For years, the Westside luxury thesis was built on a stable assumption: certain ZIP codes were structurally safer than others, and that safety was already priced in. The $52B figure dismantles that assumption in a single line item. Coastal and hillside neighborhoods that were priced as "safe" are now being repriced around two new variables — rebuild capacity and insurability — that didn't materially affect appraisals five years ago.

The insurance side of that equation has its own data. The California Department of Insurance's Safer from Wildfires regulation requires every admitted carrier in the state to offer discounts when a home adopts any of 12 specific mitigation measures, from Class A roofs to ember-resistant vents to a 5-foot non-combustible Zone 0 perimeter. Stack those measures into IBHS Wildfire Prepared Home Plus certification, and Mercury Insurance, among others, has published wildfire premium reductions of up to 50%. The math is no longer abstract: the insurability of the structure now shows up directly in the carrying cost of the asset.

What this means for LA's luxury market in 2026

A $52B reset in residential damage forces three structural shifts in how luxury LA trades. First, lots and tear-downs in fire-exposed ZIPs are increasingly being underwritten as build sites, not as inherited homes — buyers are pricing in the cost and timeline of constructing something that will be insurable at delivery, not just permittable. Second, comparable-sales analysis is fragmenting: a wood-frame rebuild and a non-combustible reinforced-concrete build on the same street are no longer the same comp, because their long-run insurance and maintenance profiles diverge sharply. Third, the buyer pool is narrowing toward UHNW principals who can afford to underwrite the construction premium required to land on the insurable side of the line — and who increasingly view that premium as a discount on the next thirty years of carrying cost.

The implication for Malibu, Palisades, Bel Air and the broader Westside is that the prestige geography is being recut. The address still matters. The structure on it now matters at least as much.

A $52 billion damage line doesn't just close a chapter on the January 2025 fires — it opens the next pricing cycle for LA luxury. The neighborhoods will recover. What's changing, quietly and permanently, is which homes inside them get to be priced as long-duration assets.