The Insurance Institute for Business & Home Safety has widened the universe of homes eligible for verified wildfire mitigation discounts by roughly two million properties, according to reporting from Digital Insurance. The expansion is the latest move in a sequence that has steadily transformed IBHS's Wildfire Prepared Home designation from a California pilot into a multi-state underwriting reference, and it lands in a market where carriers are still recalibrating after the January 2025 Los Angeles fires.

For California luxury owners, the signal is less about the certification itself and more about how insurers are choosing to read it. As the eligible footprint grows, the designation behaves less like a regional incentive and more like a baseline technical standard that underwriters can price consistently across portfolios.

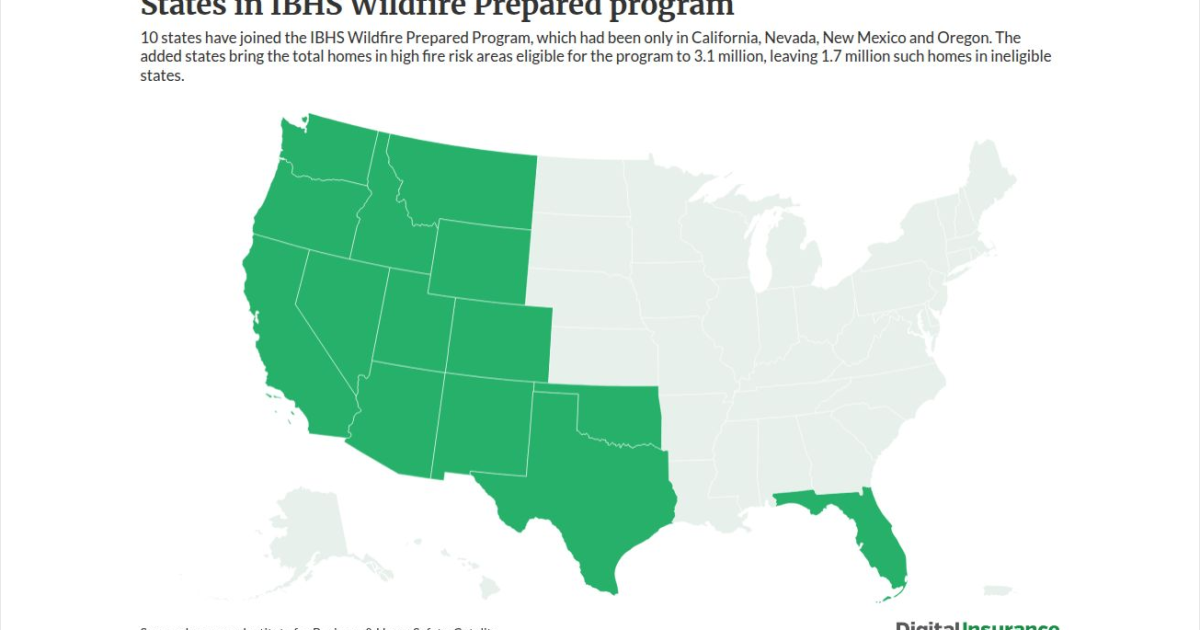

A Standard Crosses a Threshold

The Wildfire Prepared Home designation was originally launched as a California-focused program before expanding outward. With the latest extension, Digital Insurance reports that two million additional homes now sit inside the eligible map — a meaningful jump in the addressable population that carriers can underwrite against a single, externally validated checklist.

In California specifically, the IBHS designation has been folded into the broader Safer from Wildfires regulatory architecture maintained by the California Department of Insurance. Carriers including Mercury have publicly tied premium reductions of up to 50% to IBHS-certified homes, and the FAIR Plan recognizes mitigation across structure, parcel, and community layers. The combined effect is that a designation built around components — Class A roofing, ember-resistant vents, enclosed eaves, non-combustible cladding within Zone 0 — now operates as a portable financial signal that travels with the property.

Two million additional homes added to the IBHS-eligible map. Thirteen states now inside the Wildfire Prepared footprint. Up to 50% wildfire premium reduction available through participating California carriers for certified homes.

What This Means for the LA Market

The Los Angeles luxury market is the most acute test case for what a widened IBHS footprint actually does. Carriers operating across multiple states have an obvious incentive to standardize their wildfire underwriting language, because residual risk is easier to reinsure when it references a common technical standard. As the eligible map grows, the cost of being outside it becomes more visible — not because of any single new rule, but because the comparable set has changed.

For homeowners commissioning new construction in Malibu, Beverly Hills, or the Westside canyons, the practical effect is that mitigation conversations are migrating earlier in the design process. The 2026 California WUI Code (Title 24, Part 7) sets a code-level floor for new builds in Fire Hazard Severity Zones; IBHS sits above that floor as a voluntary designation that carriers can price. When the designation is rare, it is a discount opportunity. As it becomes common across millions of homes, it begins to function as the reference point against which uncertified properties are measured.

That distinction matters for any owner thinking about a custom home as a multi-decade asset rather than a single transaction. The relevant question is no longer whether a hardened envelope produces a near-term premium discount. It is whether the property will trade, refinance, and insure cleanly against a standard that is rapidly becoming the default.

Looking Ahead

A larger IBHS map does not resolve California's insurance dislocation, and it does not change the underlying pressure on the FAIR Plan or on carriers re-entering the admitted market. What it does is push the conversation about wildfire risk further upstream — into engineering decisions made on day one of a project rather than retrofits negotiated at renewal. For 2026 and the years immediately after, that upstream movement is likely to be the most consequential development for owners specifying new luxury construction in Los Angeles.